Let’s talk about John.

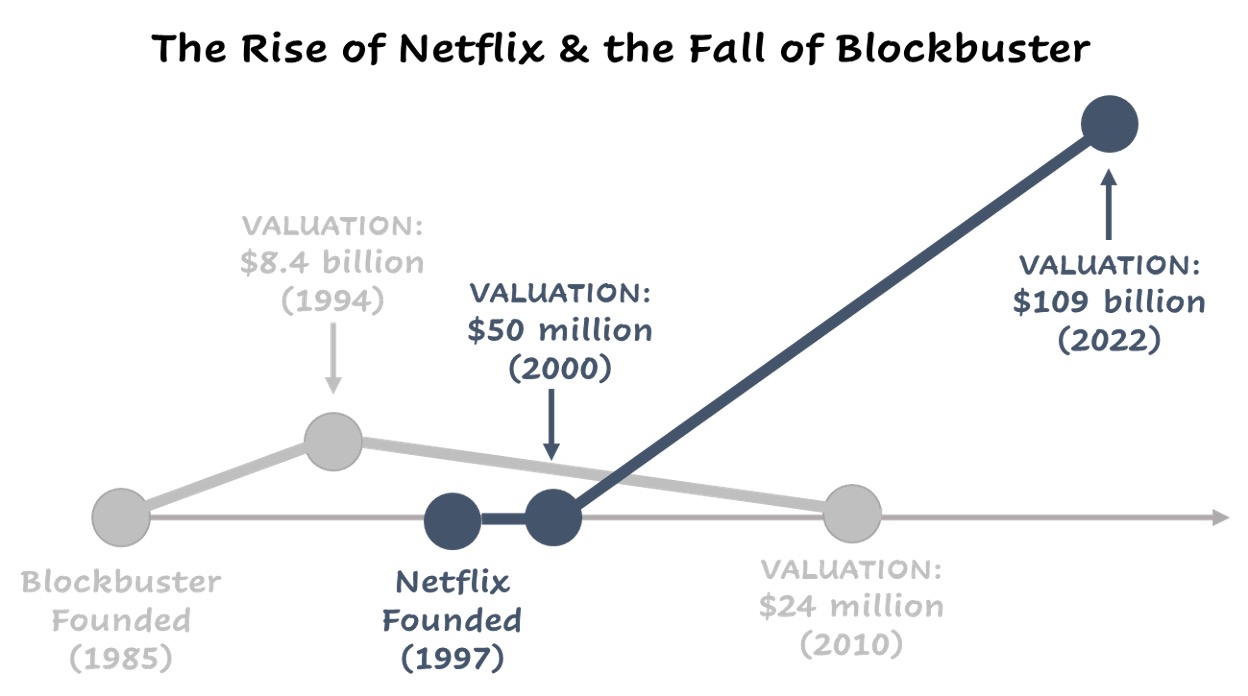

John was the CEO of a media company – his company had approximately 8,000 stores, operated in the US, Europe, Latin America, Australia, Canada, Mexico, and Asia, and employed 58,561 people. Everything was going great – people could not get enough of John’s company’s services and his company was the king and it looked like it would remain the king in times to come.

One fine day in 2000, John went into a peculiar meeting – the CEO of a novice media company thought that it was better to be a part of John’s company than fight for market share and thus, was offering up his enterprise as an acquisition for $50 million. John laughed. To think that a 3-year-old company founded based on a fad could think they would give any competition whatsoever to John’s company and would dare to put a $50 million price tag on itself was not just foolish, but laughable. Naturally, John passed on the offer.

In 2010, John’s company filed for bankruptcy.

In 2010, Reed, the CEO who had offered up his company on a silver platter 10 years earlier – his company had 20% of John’s company’s market and was signing deals with the likes of Sony, Paramount, Lionsgate, and Disney.

John’s company? Blockbuster. John Antioco.

Novice company? Netflix. Reed Hastings.

Source: The Best Acquisitions of All Time | History and Strategy | Deep Podcast Case Studies (acquired.fm)

Post their 2000 meeting with Netflix, it took 4 years for Blockbuster to realize that Netflix’s online subscription-based service posed a significant threat to their business and in 2004, they launched their own online platform at a cost of $200 million and allocated another $200 million to drop late-fees from their business model to remain competitive.

Why give your business an inorganic push?

Blockbuster. Excite. Kodak. Western Union. Mars. Groupon.

What do all these names have in common?

Once upon a time, all of them were massive successes in their respective fields, if not the market leader. Each was approached by an opportunity eager to be exploited. Blockbuster by Netflix; Excite by Google; Kodak by Steven Sasson; Western Union by Alexander Graham Bell; Mars by E.T.; Groupon by Google. However, each of these companies turned away the proposition and later, succumbed to market pressure and either went bankrupt or fell from their king-like stature. So, what should you do to avoid such a fate?

Simple. BE AWARE and embrace inorganic growth.

You see, the 21st century is marked by rapid technological innovation and evolving consumer preference – in this fast-paced environment, businesses which do not embrace change and unlock value with every move, die. Every second counts. While the traditional and common perspective is that organically achieving growth is the one true strategy. It is safe, controlled, sustainable and perhaps, cheap, what one cannot deny is that it is unbelievably slow. Either be a genius and decipher a shift right at the beginning or by the time you reach at a stage to exploit innovation “A” through all your plans and all the money you spent, it is already old, and it is now time for innovation “B”. Not to mention, no matter how talented founders are, there will always be something called the capabilities glass-ceiling.

This is where inorganic growth comes into play.

Diving into Inorganic Growth

Inorganic growth is when you look outside your own business to grow, by collaborating with other businesses. It employs either of two strategies:

a) Partnership & Licensing

Partnerships & licensing are best employed when without giving up full control of your own business or wanting to deal with the cumbersomeness of managing the operations of another business, you just leverage the most complimentary bits of each other to the best possible outcome. For instance, Uber & Spotify have a strategic alliance in place wherein riders are allowed to stream their playlists whenever they take a ride. While this lends a personalized experience to Uber and gives it a competitive edge over its peers, for Spotify, it encourages new customer growth. Similarly, Starbuck’s partnership with Target and Barnes & Noble allows it to host its counter in each of their stores and increase sales for all involved.

b) Mergers & Acquisitions.

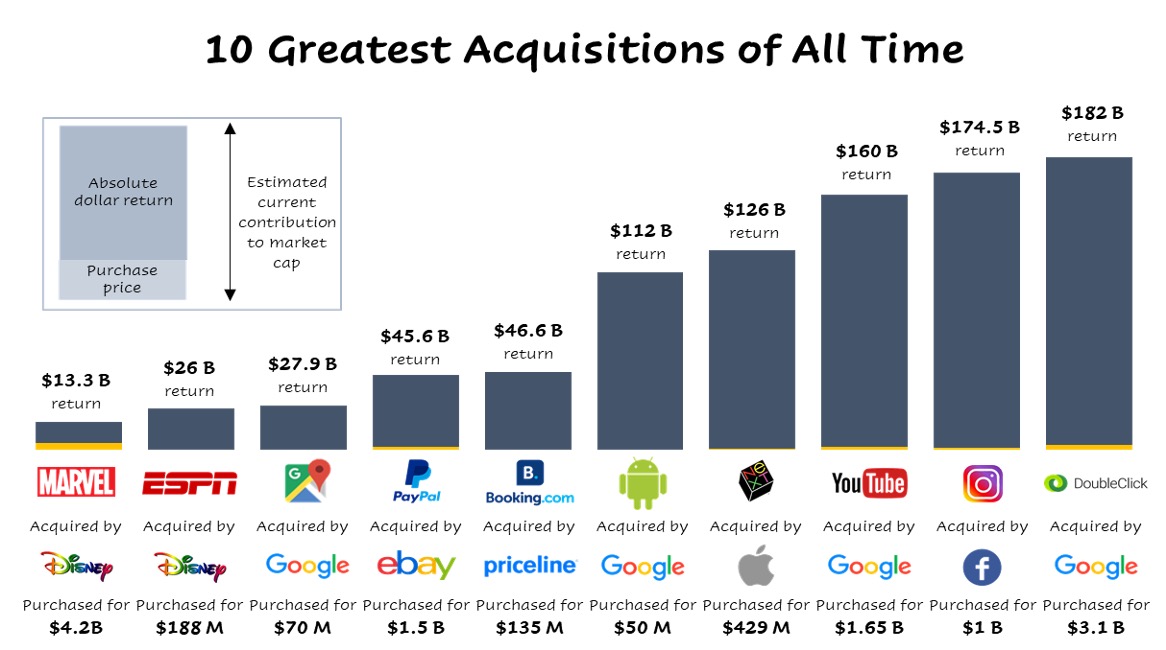

On the other hand, mergers and acquisitions are adopted when the entire business of another company complements or supplements yours. For instance, Disney has been actively acquiring leading production companies – Pixar’s acquisition allowed it to add the world’s most advanced animation practices, Marvel and Lucasfilm’s acquisitions allowed Disney to acquire large movie franchises and merchandising rights to films that could be marketed via its retail branches; and with 20th Century Fox, Disney acquired an enormous back catalogue. Similarly, when Boeing acquired EnCore Group, it took a step towards vertical integration by adding aerospace manufacturing to its portfolio and keeping the same in-house to reduce costs.

While the target of both, organic and inorganic growth are the same – increasing shareholder value, improving profits by way of increase in market share, acquiring more customers, adding more products, more offices/facilities, acquiring talent and intellectual property, vertical integration, new business model, geographic expansion etc., the glaring difference between both is the pace with which inorganic growth can be implemented.

More about Acquisitions

Most business owners have a love-hate relationship with mergers and acquisitions – they fear the unknown and the threat of failure. However, M&A is the classic example of “greater the risk, greater the return”. If implemented properly, acquisitions have the potential of disrupting industries and adding tens of thousands to a company’s bottom line.

Source: The Best Acquisitions of All Time | History and Strategy | Deep Podcast Case Studies (acquired.fm)

- Planning

The first step before entertaining M&A is thinking and thinking hard. What is the problem that needs to get solved? We obviously are looking for growth but growth via what? Are we looking for a deal which helps us improve our margins? Or a company which helps us gain a larger market share? Or is our target to expand our product portfolio and service offering? Or maybe we think that we should vertically integrate? Or maybe an acquisition which allows us to buy some innovation at a cost cheaper than it would take to develop it? Or we may be thinking about leveraging their talent pool? ‘Beginning is half done’ and just identifying the intention certainly helps streamline the path ahead and keeps a check on the initiatives undertaken.

- Target Identification

The next step would be to identify a target. Now this depends upon your strategic intention – if you want to gain a larger market share via consolidation, either a series of small acquisitions would work the best or a few large ones; on the other hand, there may be a small-sized tech firm in need of funding developing the very technology you use that you could acquire to access that. In quite a few cases, especially when it comes to innovation, value creation is maximized when acquiring a business which is early in its lifecycle or maybe, is undervalued. Synergy is a particularly important term to be kept in mind when making this decision – it simply means that the best business combination should result in benefits greater than those involved individually or 2 +2 should definitely be as much greater than 4 as is possible.

- Due Diligence

The third step is to conduct the necessary due diligence with utmost, well, diligence! Half of the failed M&As out there would actually be individual success stories had their management “diligently” conducted this step and paid heed to any red flags thrown out during the process. It is also necessary to keep in mind that these red flags would not always be quantifiable – for instance, while the Volvo-Renault merger had potential red flags right from the start – the integration of investor-owned business with a government owned one which would have left the government in charge with a 65% ownership of a profit-focused business, the Daimler-Benz and Chrysler merger failed because of cultural differences – while one had a structured culture, the other one had an entrepreneurial one and manager clashes were gossip-worthy!

- Integration

Integration is the last step to completing a M&A and dealt with best if the individuals responsible for due diligence participate in this process. The key to integration is keeping sight of the strategic intention, setting targets, identifying risks, having a tailored plan of action, taking staunch firm decisions, and never ever losing out on the key people!

The Times to Come

The above practices sound heavy and they are. They are what distinguishes a success story from a failure. Even though it looks like COVID finally is a thing in the past, the Ukraine war is keeping an environment of uncertainty alive – add to it a backdrop of rising global inflation, interest rate hikes and increased regulatory hurdles, businesses, now, more than ever, need to fight to keep themselves on the growth path.

2021 marked the best year global M&A has ever witnessed with deal volume at its highest and deal value surpassing $5 trillion for the very first time. For the North American market too, 2021 was a record year with approx. 17,917 disclosed deals and $2.7 trillion in deal value. However, dampened by the macroenvironment, deal activity in H1 2022 has not even been half of that witnessed in 2021 – but all is not bad – given it is nearing its pre-COVID strong levels, looks like what is actually changing, is strategy.

Source: Q2 2022 Global M&A Report | PitchBook

According to a Deloitte survey, out of all businesses looking out for a M&A, 61% are adopting a defensive approach and the rest are on offensive – eager to scale the world. Additionally, an increasing proportion of businesses are looking out for divestitures to optimize their portfolio. With rising interest rates increasing the cost of capital for acquirers and increasing the pressure on generating significant returns, mega deals have declined. Business environment has also paved way for lower valuations.

An analysis by EY reveals that economic slowdown is one of the best times to add compounded value to your company. Companies that actively engage in M&A during the downturn outperform those which do not by an average of approx. seven percentage points – this is over a three-year period. If we look at the five-year analysis, active acquirers benefit by an average of approx. twelve percentage points than other companies!

Even if you are not a glass half-full type of person, what more, I ask, would you consider a perfect environment for an acquisition? Hence…

Sources: