The world of DeFi (Decentralized Finance) has been on a steady rise for the past couple of years. First came into existence as a solution for the strictly regulated traditional finance space, DeFi is now considered a significant area in the finance sector. So much so that major companies and banks are experimenting in DeFi with major capital and governments across the world are looking into probable regulations.

So how did all these come about in just half a decade or less, we’ll explore that in this article.

Generally, in traditional finance, a bank works as a middleman in any transaction process. The same happens with lending/borrowing, the banks decide who to lend to by setting up a number of eligibility criteria. While borrowing money from banks is an animal of its own, lending money is something even more difficult in traditional settings without exposing yourself to high-risk parameters. DeFi solves these problems

What is DeFi?

The idea of DeFi first came about after the invention of the Ethereum blockchain. The first blockchain was programmable and could host other applications (dApps) on top of it. The idea, in the beginning, was a simple one. Peer-to-Peer (P2P) lending.

In P2P lending/borrowing scenarios, a person who wants to lend money sets up a list of T&C in a smart contract, which a borrower needs to agree to for them to get the money. If both sides agree, a smart contract gets executed and recorded in the blockchain and the transaction gets completed. However, the issue with this is efficiency. A system like this is simply not scalable when every borrower/lender has to find a perfect match. As a result, the next step in DeFi was Liquidity Pool.

A liquidity pool is a pool of crypto assets (sometimes specific like ETH/BNB, sometimes not) where any lender can put their money for interest. Anyone who wants to borrow the money needs to put in collateral (more than the amount borrowed) to take out a loan. Although there’s a lot more to it than that, it’s enough to explain the process. If anyone defaults on the loan, the collateral gets liquidated and the lenders are compensated proportionally.

Most popular DeFi platforms

The most popular and reliable DeFi platforms are Aave, Maker, Compound, Uniswap, Bancor, Curve, etc. However, the two most important DeFi platforms that helped establish DeFi into what it is today are Maker and Aave. Built on Ethereum, MakerDAO first introduced the concept of liquidity pool and overcollateralized loans. Unlike banks where the collateral barely meets the value of the loan, in Maker, the value of the collateral must be 150% of the value of the borrowed amount.

So if you borrow $100 worth of ETH, you’ll have to put down $150 worth of ETH at the minimum. If the limit goes below 150% in any situation, the smart contract will liquidate the whole collateral to safeguard the lenders. Maker also introduced the native stablecoin DAI, which is pegged 1:1 to the USD. On the other hand, Aave revolutionized DeFi with Flash Loans. Flash loans are basically collateral-less loans where you need to borrow and repay the loan within the standard Ethereum block time of 13 seconds. Flash loans are useful in particular scenarios like Arbitrage, Collateral Swap, and Self Liquidation events.

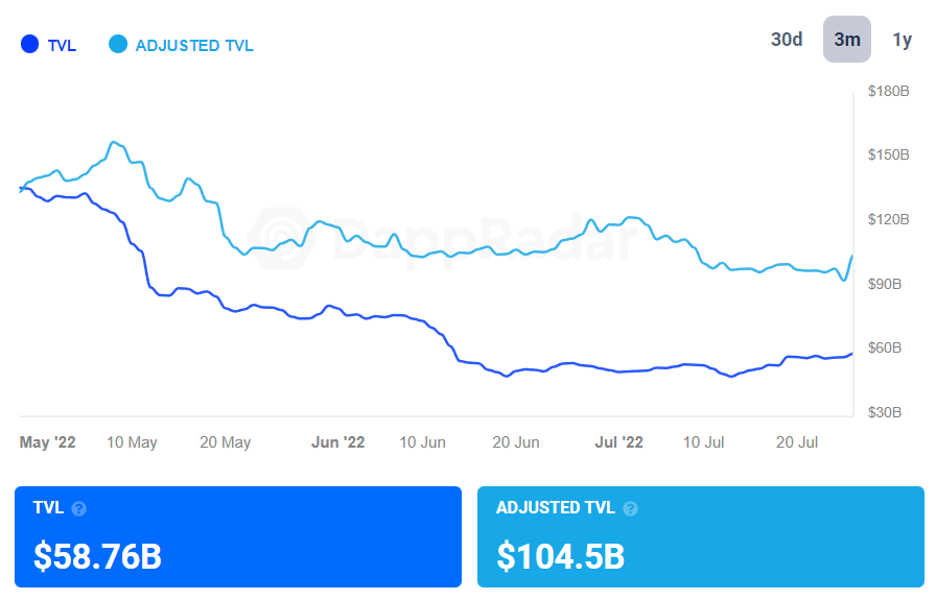

The current state of DeFi

DeFi has been on the rise with the popularity of new platforms like Lido, Oasis, and several others. Also, platforms like Synthetix have been experimenting with DeFi derivatives and synthetic assets which can become a powerful instruments in the future. Although the current market crash and the looming possibility of a crypto winter have affected the market quite a bit.

Source- Dappradar

The collapse of Terra Luna, Celsius, Voyager, and 3AC capital has pointed out several flaws in the system and how risky practices can put public assets in danger. There’s no denying that these platforms and several others have sent out a ripple effect across the whole market and compelled builders to look closely into the issues.

However, the fundamentals of DeFi is strong and as the cycle comes to an end, we will have a better understanding of how resilient the new finance sector is and how relevant it will remain.